Private equity pay in 2026 is still elite, but the mix (base + bonus + carry) and the MM vs. mega‑fund split matter more than any one number you’ve seen on forums. Below you’ll get 2026 ranges by level, how bonuses actually hit, and a dead‑simple way to estimate carry, plus why a faster promotion path in MM can beat a higher year‑one paycheck at a mega‑fund.

- Associates: $275k–$450k all-in cash (MM vs. MF)

- VPs: $400k–$700k cash + carry begins

- Principals: $575k–$1.2M + meaningful carry

- MDs: $900k–$3M+ cash + multi-percent carry pool

Ready to break in? Get the complete toolkit:

Download Resume Template →💰 2026 Compensation Calculator

Estimate Total Cash + Carry EV (Expected Value)

*Logic & Assumptions: Cash uses band midpoints. Carry EV applies a 90% “net investable capital” factor and assumes points are % of the carry pool. Ignores waterfall details (catch-up/clawback, European vs deal-by-deal). Fund sizes are illustrative ($1B / $10B baseline). Uses a simplified “pref proxy” (8% over 5 years) to gate the hurdle. Annualized over a 10-year fund life (“dollars at work” framing) for comparison, though actual payout is lumpy and exit-driven.

Get the full negotiation playbook (PDF)

Get Deal Flow Bullet — free, every Friday. Join 100+ MM practitioners.

Private Equity Salary Overview 2026

📊 Middle-Market Cash Compensation (2026)

Directional bands for U.S. middle-market buyout funds (~$0.5–3B AUM). Cash comp = base salary + annual bonus; carry shown separately.

| Level | Base Salary | Bonus (% of base) | All-in Cash |

|---|---|---|---|

| Associate | $155k – $170k | ~75% – 125% | ~$275k – $350k |

| Senior Associate | $170k – $200k | ~80% – 140% | ~$300k – $480k |

| Vice President | $200k – $240k | ~100% – 160% | ~$400k – $620k |

| Principal/Director | $275k – $325k | ~100% – 200% | ~$575k – $950k |

| MD/Partner | $350k – $500k | 150%+ | ~$900k – $2m+ |

*Analyst roles are still relatively rare in true MM/LMM; most analyst seats sit at upper-middle-market and mega-funds.

Middle-Market vs. Mega-Fund Comparison (Click to expand)

| Level | Middle-Market | Mega-Fund | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Base | Bonus% | All-in | Carry Start | Promo | Base | Bonus% | All-in | Carry Start | Promo | |

| Analyst | —/rare | — | — | — | — | $110–145k | 40–70% | $160–225k | — | 2–3y |

| Associate | $155–170k | 75–125% | $275–350k | SA/VP | 2–3y | $165–180k | 90–140% | $325–450k | SA/VP | 2–3y |

| Sr. Associate | $170–200k | 80–140% | $300–480k | VP | 1–2y | $180–210k | 100–150% | $360–525k | VP | 1–2y |

| Vice President | $200–240k | 100–160% | $400–620k | VP ✓ | 2–3y | $220–260k | 100–170% | $450–700k | VP ✓ | 2–3y |

| Principal | $275–325k | 100–200% | $575–950k | Principal | 2–4y | $300–375k | 120–220% | $700k–1.2m | Principal | 2–4y |

| MD/Partner | $350–500k | 150%+ | $900k–2m+ | 2–8% pool | — | $400–600k | 150%+ | $1.2m–3m+ | 2–8% pool | — |

Ranges vary by firm performance, city, sector, and fund size. Cash comp excludes carry. *Analyst roles are mostly MF/UMM; relatively uncommon in MM/LMM (but growing).

Methodology & Sources

Compensation ranges reflect aggregated recruiter conversations, public survey snapshots, and anonymized datapoints across 2024–2025. Cash comp = base + annual bonus. Carry is shown separately because of vesting and realization timing.

- Adjusters: fund size/strategy, city, sector focus, and firm performance materially shift outcomes.

- Rounding: Bands are rounded to practical hiring brackets; examples are illustrative only.

- Currency & timing: USD; last updated .

This page is for education, not individualized advice. Send corrections here and we’ll update promptly.

Let’s be real: the private equity industry is hitting some serious compensation peaks in 2026, with associate base salaries climbing to $165k-$180k and total comp packages reaching $430k+ at top firms. This isn’t just another “cost of living adjustment”—we’re talking about the most aggressive salary growth the industry has seen since those post-2008 talent wars, driven by record dry powder levels exceeding $3.5 trillion globally and some pretty fierce competition for investment professionals. And yeah, bonuses increased significantly in 2026 too, further boosting total comp and reshaping the whole private equity salary landscape.

But here’s what most salary guides won’t tell you (and what I wish someone had told me when I was grinding it out): base salary is just the appetizer. The real wealth creation in private equity comes from carried interest, which can transform a VP’s $250k base into multi-million dollar annual payouts when funds actually perform.

Understanding this comp architecture isn’t just academic stuff—it’s literally the difference between optimizing for short-term cash and building generational wealth. Megafunds essentially set the top comp expectations and benchmarks for the industry; this then trickles down to the MM to LMM.

This guide breaks down exactly what every level earns in 2026, from first-year analysts to managing directors, and more importantly, reveals the strategic decisions that can 10x your lifetime earnings in this industry.

Carry 101 (with simple math)

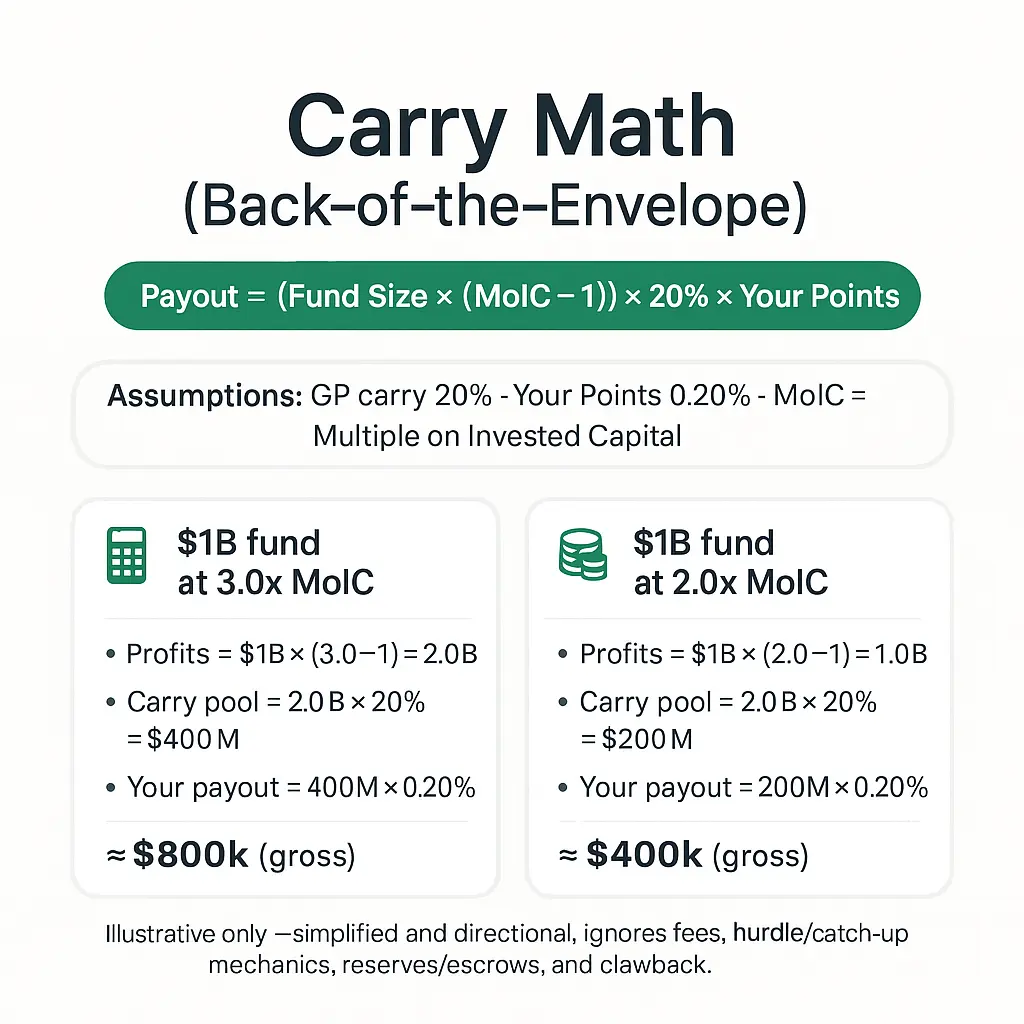

Carried interest (“carry”) is the cornerstone of private equity compensation and the key driver of long-term wealth for senior professionals. In buyout PE, carry is usually 20% of profits net of fees and expenses per the LPA—paid only after limited partners have received their invested capital back plus a preferred return (commonly an ~8% hurdle). Higher percentages (25–30%) exist but are uncommon and strategy-specific (e.g., some VC or smaller funds).

Carry 101 (with simple math)

🎯 The Carry Formula

Carried interest (“carry”) is the cornerstone of PE wealth. Here’s the back-of-the-envelope math:

Payout ≈ (Fund Size × (MoIC − 1)) × Carry% × Your Points

- Example A (3.0× return): $1.0B fund → profits ≈ $2.0B; 20% pool ≈ $400M

At 0.20% points → ~$800k over fund life - Example B (2.0× return): $1.0B fund → profits ≈ $1.0B; 20% pool ≈ $200M

At 0.25% points → ~$500k over fund life

Your carry points represent your share of this 20% pool, not a percent of the fund size or total profits.

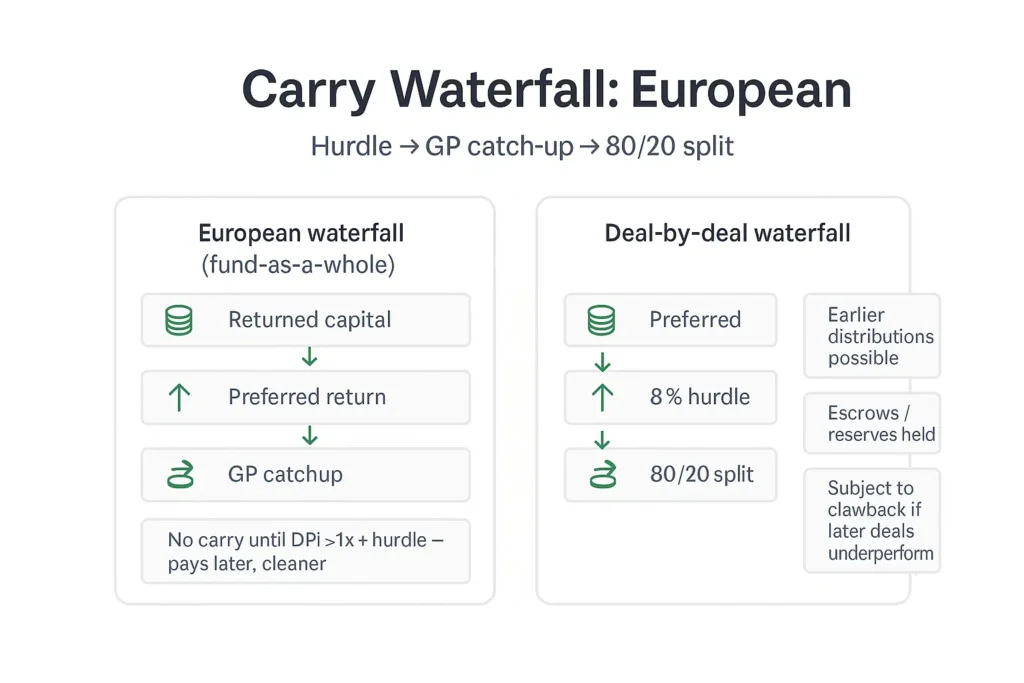

Distribution waterfall (fast)

Hurdle rate: Limited partners receive their invested capital plus a preferred return (usually ~8%) before carry is paid.

GP catch-up: General partners receive a larger share of profits after the hurdle is met until they “catch up” to their full carry percentage.

Distribution method: Funds may use a European (fund-as-a-whole) or deal-by-deal approach, with the latter often involving escrows or reserves to manage risk and timing of carry distributions.

Clawback provisions: Protect limited partners by requiring general partners to return previously distributed carry if early distributions exceed their ultimate entitlement.

Vesting & timing: Carry points typically vest over 4–6 years (often cliff + straight-line) and pay only on realized exits. Unvested points usually forfeit on departure

VP Level

~0.1–0.5%

First meaningful carry

Principal/Director

~0.5–1.5%

Significant step-up

Partner/MD

Multi-%

Share of carry pool

Co-Invest 101: Small Checks, Real Upside

📌 Access

More common at VP+; some shops open small tickets to SAs

💰 Typical Size

$10k–$100k per deal (firm & compliance dependent)

📊 Terms

Often pari passu with fund; sometimes limited leverage via employee program

⚠️ Risk

Single-asset exposure, illiquid, capital calls can arrive during dry spells

Private Equity Compensation by Position Level

Career Roles & Responsibilities Quick Reference

- Analyst: Builds models and diligence modules, supports IC. Typical runway 2–3 years to Associate; carry rare.

- Associate: Owns workstreams end-to-end (screening → DD → close), coordinates advisors, starts portco projects.

- Senior Associate: Leads diligence modules, mentors juniors, drafts IC narratives; some firms pilot small points.

- Vice President: Runs processes, begins origination, manages CEO/banker relationships; first meaningful carry at many funds.

- Principal/Director: Origination engine + IC leadership, sector strategy, team development; carry steps up.

- MD/Partner: LP relationships & fundraising, firm strategy, exit leadership, and governance.

Private Equity Analyst Salary 2026

Base / Bonus / All-in: $110–145k base; ~$50–80k bonus → ~$160–225k all-in

Where these roles live: Mostly UMM/mega-funds; selective spots at a few MM firms

What moves you up: Clean, independent diligence workstreams, bullet-proof models, crisp IC materials

Progression & equity: 2–3 years to Associate or MBA; carry is rare; occasional small co-invest

The analyst role is the entry point at mega-funds and select middle-market shops, typically recruiting from top undergraduate programs with strong internship experience. While finance and banking pipelines still dominate, some firms are increasingly open to non-traditional candidates (e.g., consulting or technical backgrounds) who can contribute immediately to diligence and market work.

Bonuses vary with firm performance and your direct contribution to deal execution. Analysts who run tight workstreams—accurate models, airtight diligence memos, and clear IC exhibits—tend to land at the top of the band.

Most analysts spend 2–3 years in seat before promoting to Associate or heading to business school. A few firms offer small co-invest opportunities, but true carry at this level is uncommon. Core skills to prioritize: advanced modeling, process management, and portfolio KPI tracking.

In 2025 some funds introduced fast-track promotions for exceptional performers. If you can independently manage diligence modules and materially improve IC readiness, you may move ahead of traditional timelines.

The analyst gig? It’s still your golden ticket into the mega-funds and those select middle-market shops that actually matter, and they’re laser-focused on snagging candidates straight from top undergrad programs (preferably with internship experience that doesn’t involve making coffee). While the traditional path still heavily favors the finance and investment banking crowd (shocking, I know), some firms are finally waking up and giving non-traditional candidates a shot – think consultants who can actually build a model or technical specialists who won’t break Excel with a #REF! error.

Here’s the real talk: your bonus is going to swing wildly based on how your firm performed and whether you actually contributed to deals or just sat there looking pretty during due diligence. Analysts at the top PE shops who can whip up financial models without breaking a sweat and catch every tiny detail during due diligence (while the rest of us are struggling to stay awake) can often score bonuses at the absolute top of the range. It’s brutal math, but hey, that’s the game.

Most analysts grind it out for 2-3 years before either climbing up to associate level or bailing for business school (because who doesn’t love more debt, right?). Unlike your future associate colleagues, analysts rarely see carried interest – though some progressive firms are throwing small co-investment opportunities your way on select deals (basically breadcrumbs, but breadcrumbs that might actually pay off). At this level, you’re building the foundational skills that matter: financial modeling that doesn’t make people cry, deal execution that actually gets things done, and portfolio monitoring that keeps everyone from panicking.

Plot twist for 2026: career progression for analysts has actually hit the gas pedal, with some firms creating fast-track promotion opportunities for the absolute rock stars. Analysts who can independently manage due diligence workstreams without constant hand-holding and contribute meaningfully to investment committee presentations (instead of just nodding along) are finding themselves promoted way ahead of the traditional timelines. Translation? If you’re good, really good, you might not have to suffer through the full analyst hazing period.

Private Equity Senior Associate Salary 2026

Base / Bonus / All-in: MF: $180–210k base; ~$180–315k bonus → $360–525k all-in | MM: $170–200k base → $300–480k all-in

What drives pay: Lead diligence modules, mentor juniors, draft IC narratives

Role shift: Bridge between execution and strategy; begin relationship management

Progression & equity: Some firms offer pilot carry points (0.05–0.1%); 1–2 years to VP

Associate seats are the industry’s most competitive hiring lane, drawing heavily from investment banking and management consulting. Larger funds pay at the top of the bands, but the dispersion comes from performance—clean diligence, crisp IC materials, and tangible portco wins tend to push bonuses into the upper ranges.

The day-to-day is broad: build and own the model, coordinate advisors, drive diligence modules, and start managing external relationships (deal sources, management teams). The learning curve is steep but accelerates responsibility—especially at MM shops where teams are leaner.

After-Tax Snapshot (Illustrative)

Assume base $175k + bonus $200k in NYC. Aggregate taxes can land near ~45%, leaving ≈ $206k after tax. In Austin, take-home might be ~50–55% given no state income tax.

Not tax advice—directional bands only. Outcomes depend on filing status, deductions, and timing of carry distributions.

Let’s be real: private equity associate compensation is basically the Hunger Games of finance talent, and these folks know they’re holding all the cards (having survived the investment banking meat grinder or McKinsey PowerPoint factory, they’ve got options and aren’t shy about it). The comp gap between firms isn’t just about dollars – it’s about the golden handcuffs of working at places like Blackstone or KKR, where they can literally afford to throw money at talent like they’re buying vintage wine. These shops don’t just pay well; they pay “please don’t leave us for that hedge fund” well.

Get Deal Flow Bullet — free, every Friday.

One email a week — real deal frameworks and technical breakdowns from a middle-market practitioner. No fluff.

Bonuses for PE associates? Oh boy, buckle up. We’re talking about serious cash that’s tied to whether your fund is printing money or just burning through LPs’ retirement funds. The top-tier mega-funds are basically running a performance-driven casino where your bonus depends on deal success and how your firm stacks up against the competition (spoiler alert: everyone thinks they’re top decile). If you’re crushing it at a mega-fund during a vintage year that doesn’t suck, your bonus can literally exceed your base salary – which is both terrifying and amazing, depending on how you feel about your job security.

Here’s where things get spicy: the associate level is where PE stops being theoretical and starts being “why am I awake at 2 AM modeling EBITDA adjustments?” Unlike those poor IB analysts who spend months building one tiny piece of a massive deal (and probably never see the closing dinner), PE associates own the whole damn process from “hey, this company looks interesting” to “congratulations, we just spent $500M.” You’re building models that actually matter, schmoozing with deal sources who may or may not buy you drinks, and sitting across from CEOs trying to figure out how to make their companies worth more money (while secretly Googling industry terms under the table).

Now here’s the kicker that’ll make your future self thank you: some forward-thinking firms are starting to sprinkle a little carried interest fairy dust on associates after 2-3 years – we’re talking about 0.05%-0.1%, which sounds like peanuts until you realize it’s basically free money if you stick around and the investments don’t completely tank. Sure, it’s not “buy a yacht” money, but for associates who survive multiple fund cycles and help generate those sweet, sweet returns, this early carry exposure can turn into something actually meaningful (and gives you bragging rights at overpriced cocktail bars).

Private Equity Vice President Salary 2026

Base / Bonus / All-in: $200–260k base; ~$200–440k bonus (100–170% of base) → $450–700k total cash

Carry starts here: Typically 0.1–0.5% points of the carry pool; $1B fund at 3.0× with 0.20% points ≈ $800k over fund life

Role inflection: Run processes end-to-end, begin consistent origination, translate operating levers into value creation

What top VPs do: Build repeatable sourcing pipeline, spot pattern risk in diligence, coach teams, maintain CEO-level trust

Role inflection: VPs run processes end-to-end (advisor orchestration, SPA/credit docs, IC calendars), begin consistent origination, and translate operating levers (pricing discipline, go-to-market, KPI cadence) into underwriting and value-creation plans.

What top VPs do: build a repeatable sourcing pipeline, spot pattern risk in diligence, coach associates/SAs, and maintain CEO-level trust. Communication with management and LPs becomes central to the seat.

The vice president level represents a major inflection point in private equity careers, both in terms of compensation and wealth-building potential (this is where things get seriously interesting, and your parents might finally stop asking when you’re getting a “real job”). The real differentiation comes in bonus potential and, critically, carried interest eligibility – which is basically where you stop being just another highly-paid analyst and start building actual wealth.

VPs are expected to take ownership of deal processes and begin developing their own network of deal sources (translation: you can’t just wait for deals to land in your inbox anymore). The most successful VPs in 2026 are those who can combine traditional private equity skills with operational expertise, particularly in areas like digital transformation and ESG implementation across portfolio companies. Let’s be real – if you’re still just cranking models at the VP level, you’re missing the point entirely.

In addition to financial modeling and deal execution, VPs must excel at managing relationships with portfolio company executives and limited partners (and trust me, these conversations are way more fun than explaining DCF assumptions to your MD for the hundredth time). Strong communication skills and strategic thinking are essential as VPs often represent the firm in external negotiations and investor meetings. The ability to navigate complex market dynamics and identify emerging investment opportunities in key financial hubs is increasingly valued – because unlike associates, you actually get a seat at the table where decisions happen.

Given the competitive landscape for new talent, private equity firms are placing a premium on VPs who demonstrate leadership in sourcing proprietary deals and driving superior fund performance (spoiler alert: this is where you prove you’re not just another banking refugee). Those who can blend investment banking experience with a deep understanding of industry trends and operational improvements command higher compensation and faster career progression. It’s like having your cake and eating it too, except the cake is made of carried interest and the eating part involves actually creating value for portfolio companies.

Moreover, VPs often play a key role in mentoring associates and senior associates, helping to build cohesive investment teams that can execute complex transactions efficiently (congratulations, you’re now officially responsible for making sure the next generation doesn’t blow up any models). This leadership responsibility further distinguishes high-performing VPs and contributes to their higher bonuses and carry allocations. Think of it as your chance to be the VP you wish you’d had when you were grinding away as an associate.

Overall, the VP level marks a critical stage where compensation shifts from primarily salary and bonus towards meaningful carried interest participation, aligning long-term incentives with fund success and personal wealth creation (and yes, this is where you can finally afford that apartment without three roommates). It’s the moment when your career transforms from trading time for money to building actual equity in your professional future.

Private Equity Principal/Director Salary 2026

Base / Bonus / All-in: $275–375k base; ~$425–825k bonus (100–220% of base) → $700k–$1.2m cash

Carry step-up: Typically 0.5–1.5% points; in strong exit windows, carry can dwarf cash comp

Seat shift: Origination and IC leadership dominate; sector depth, CEO-level operating cadence, team building

Success signals: Proprietary pipeline coverage, hit rate to LOI/close, realized exits, portco KPI uplift

At Principal/Director, the focus shifts from primarily executing deals to consistently originating them and shaping fund strategy. You lead diligence agendas, own IC narratives, and set the operating rhythm with CEOs—while developing associates/SAs into reliable process owners.

Carry meaningfully steps up here. Because allocations are points of the carry pool (not of total fund profits), outcomes scale with fund size, MoIC, and realization timing. Over multiple vintages, distributions in strong exit periods can exceed annual cash compensation by a wide margin.

So you’ve made it to principal or director level – congrats! You’re now in the senior investment professional tier, which basically means you get all the fun stuff: significant responsibility for fund performance, team development, and (let’s be real) some pretty serious pressure that might make you question your life choices at 2 AM. This is where you genuinely start transitioning from being the person who executes deals to the one who actually originates them and shapes fund strategy (finally, right?).

Here’s where things get interesting – carried interest allocations absolutely explode at the principal level, typically ranging from ~0.5%–1.5% points of the carry pool (that sweet ~20% share of profits we all dream about). For successful funds, this carry component can absolutely dwarf your annual cash compensation, with distributions potentially reaching $1M+ per year during those golden exit periods (and yes, you’ll probably become insufferable at dinner parties). The wealth creation potential becomes truly significant for professionals who stick it out through multiple fund cycles – assuming you don’t burn out first.

Successful principals in 2026 are the ones who can genuinely build proprietary deal flow, develop deep sector expertise that makes LPs swoon, and mentor junior team members while still maintaining their own deal execution excellence (because multitasking is apparently a superpower now). Principals and directors also work pretty closely with portfolio company executives to implement strategic initiatives and drive company growth, leveraging operational expertise to create value post-investment – basically, you become the person who has to explain why the numbers aren’t hitting projections.

Private Equity Managing Director Salary 2026

Base / Bonus / All-in: $350–600k base; 150%+ bonus → MM: $900k–$2m+ | MF: $1.2m–$3m+ cash

Carry dominance: Multi-percent share of carry pool; strong exit periods can reach eight figures annually

Seat priorities: LP relationships & fundraising, firm strategy, senior hiring, exit leadership, governance

Success signals: DPI/TVPI trajectory, realized exits, fundraising close rate, CEO/board selection quality

At MD, compensation skews away from salary/bonus toward realized carry. Cash bands vary widely with fundraising momentum and realizations, but the durable wealth engine is participation across multiple vintages and clean distribution waterfalls.

Day to day, MDs set investment agenda and culture, win capital from LPs, choose and support CEOs, and lead exits. The role blends deal judgment with institution-building: ensuring underwriting discipline, maintaining portfolio KPI cadence, and developing the next generation of partners.

Managing directors sit at the apex of private equity compensation, with packages that can reach eight figures in exceptional years (yes, you read that right – and no, that’s not a typo from someone who’s been staring at Excel too long). However, base salary represents a smaller percentage of total compensation compared to junior levels, which is honestly a pretty nice problem to have when you’re already pulling in more than most people’s wildest lottery fantasies.

Annual bonuses for MDs are highly variable and closely tied to fundraising success and fund performance (because apparently God forbid we tie compensation to actual results, right?). Managing directors who successfully close major funds or generate exceptional investment returns can earn bonuses several times these ranges – we’re talking “buy a small country” money here. Compared to senior bankers at investment banks, managing directors in private equity often see higher total compensation, especially when factoring in carried interest. Senior bankers, particularly at elite boutique firms, may receive substantial bonuses, but recent trends show that private equity MDs can absolutely crush them in overall earnings, especially during strong fund performance years (sorry not sorry, banking bros).

The real wealth creation for managing directors comes through carried interest, because let’s be honest, this is where the magic happens and dreams are made of. Large successful funds’ carry distributions can reach $10M+ annually during peak exit periods, which is basically like winning the lottery except you actually worked your tail off for decades to get there. Many managing directors earn more from carry than from their combined base salary and bonus, which is honestly a pretty nice problem to have (and probably the kind of “problem” that makes your high school guidance counselor weep with joy).

Managing directors in 2026 are increasingly focused on ESG integration, operational value creation, and managing relationships with limited partners who are demanding more transparency and accountability (because apparently investors want to know where their billions are actually going – shocking, I know). The most successful MDs are those who can balance traditional deal-making skills with modern fund management and stakeholder relations capabilities, essentially becoming part dealmaker, part therapist, and part fortune teller all rolled into one slightly caffeinated package.

Key Factors Affecting Private Equity Salaries (2026)

Firm Size & Strategy

When it comes to PE pay, fund size is the undisputed king. The massive upper-middle-market and mega-fund platforms ($3B+ AUM) have the firepower to pay a ~15–25% premium over their middle-market peers, thanks to their ability to command higher fees and attract huge LP commitments. In real-world terms, the same Associate or VP role can easily clear an extra $50k–$100k per year at a top-tier firm compared to a ~$1B shop.

Fund Size Gradient at a Glance

| Scale | Cash Comp (Assoc → VP) | Carry Timing |

|---|---|---|

| LMM (<$500m) | Lower bands | VP standard; Sr. Assoc. pilots rare |

| MM ($0.5–3B) | Mid bands | VP common; some Sr. Assoc. pilots |

| UMM/MF (>$3B) | Upper bands | VP standard; larger pool, thinner points |

Beyond raw size, elite specialized funds often pay a premium. Private equity firms with killer track records in hot sectors (like software or healthcare) can pay top-of-market because their results speak for themselves. And while larger funds boast massive carry pools, remember the individual points are usually thinner. True wealth creation still hinges on performance and timing your exits—not just the brand name.

Geography

The coastal mega-hubs of New York and San Francisco still pay a hefty premium, typically ~20–25% more than other markets, largely to offset the brutal cost of living. The next tier—cities like Boston, Chicago, and LA—offers a solid ~10–15% bump.

Meanwhile, high-growth hotspots like Austin, Dallas, and Miami are rapidly closing the compensation gap as more firms move in. And while remote teams exist, don’t hold your breath for a fully distributed future; most PE firms still run on face time.

Fund Performance & Deal Flow

- Bonuses mirror performance. Your bonus is a direct reflection of the fund’s recent success. Strong portfolio performance and profitable exits lead to fat bonus pools. A quiet vintage means they get lean.

- Deal flow dictates your life. A hot M&A market means grueling hours, but it’s also your best chance to prove your worth and get paid for it.

- For seniors, cash is secondary. At the Principal and Managing Director levels, the salary and bonus are nice, but the real, career-defining money is in carried interest. A few successful exits can generate wealth that dwarfs a decade’s worth of cash compensation.

Private Equity Compensation Components Explained

Base Salary

Base salary is your foundation—the predictable layer that pays the rent while you wait for performance-driven payouts. Bands step up with each promotion, with the biggest jumps at VP and Principal.

- Typical bands: Associates $155–180k; VPs $200–260k; Principals $275–375k (mega-funds anchor the top end).

- Key modifiers: geography and fund scale can swing base by ~10–25% (NYC/SF and UMM/MF price higher).

- Senior reality: at partner level, base is a smaller slice as realized carry dominates—still useful for cash-flow stability between exits.

Annual Bonus

The bonus is where performance meets pay. Unlike IB, PE bonuses are tied directly to your deal contribution, portfolio KPIs, and fund results.

| Level | Middle-Market Bonus (% of base) | Mega-Fund Bonus (% of base) |

|---|---|---|

| Associate | ~75–125% | ~90–140% |

| Vice President | ~100–160% | ~100–170% |

| Principal/Director | ~100–200% | ~120–220% |

- Top-end drivers: leading diligence, sourcing wins, tangible portco improvements, and fundraising impact push you toward the upper bands.

Carried Interest (the wealth engine)

Carry is your share of the GP’s profits. After LPs get capital back plus a preferred return (commonly ~8%), the firm keeps ~20% of remaining profits—the carry pool. Your points are your slice of that pool (not a % of the whole fund).

- When it starts: typically at VP. Some firms offer small Senior Associate points to top performers—perk, not standard.

- Vesting & payout: vest over 4–6 years (often 1-year cliff + straight-line) and pay only on realized exits, not paper marks.

- Back-of-the-envelope math:

Payout ≈ (Fund Size × (MoIC − 1)) × 20% × Your Points(MoIC = Multiple of Invested Capital). Example: a $1B fund at 3.0× → profits ≈ $2.0B; 20% pool ≈ $400m; at 0.25% points ≈ $1.0m over fund life. See Carry 101. - Signing / relocation: bridge forfeited bonus or timing gaps.

- Co-invest access: invest alongside the fund—ideally fee/carry-free—with clear caps.

- Deferred comp: more common at larger funds; know vesting and forfeiture rules.

- Learning budget: executive coaching, certifications, and exec-ed that compound your value.

Benefits That Actually Move the Needle

Skills & Qualifications for Private Equity Careers

Breaking into PE is a high-bar sport. The good news: the bar is visible. This section frames the standard at top funds, shows you how to signal it, and gives you a concrete plan to level up—so you’re not guessing what “good” looks like.

🎯 What Gets You Hired (and Promoted)

- Rock-solid technical core: this is the price of admission. You should be able to build an LBO from scratch, link three statements, handle debt schedules, and sanity-check returns (IRR/MoIC). Add QoE literacy and credible downside cases so your models survive IC scrutiny.

- Process ownership: run clean diligence workstreams end-to-end—coordinate advisors, manage the VDR, track issues, and hit IC calendars without drama. Basic SPA/credit-doc familiarity keeps docs moving instead of stalling at signatures.

- Operating edge: translate spreadsheets into outcomes. Pull the levers that move value—pricing discipline, GTM focus, margin expansion, cash conversion—and install a KPI cadence with portfolio teams.

- Sourcing engine: build banker/founder loops, keep a tight CRM, and maintain a repeatable funnel from intro → qualified screen → LOI. Origination isn’t magic; it’s cadence plus credibility.

- Executive-caliber communication: deliver a one-slide “so what,” frame risks and alternatives, and earn CEO/board trust. Attribute impact without grandstanding.

- Judgment & integrity: protect the downside, escalate early, and never trade reputation for a quick win. Partners notice.

Own the workstreams that move deals and KPIs. Do that consistently and compensation follows.

Your “Proof Pack” — Show, Don’t Tell

Recruiters and partners believe artifacts more than adjectives. Assemble a light, airtight portfolio you can share safely.

- Redacted IC memo: thesis, underwriting edge, key risks, and how you mitigated them—no confidential numbers.

- KPI lift dashboard: before/after metrics you moved (ARR, churn, gross margin, cash conversion) and your role in the change.

- Deal log (concise): pipeline → diligence → close; your responsibilities, decisions made, and outcomes; include manager references.

- One 2-page pitch: a recent long or deal thesis with catalysts and a simple risk/reward tree.

Redact anything sensitive. The goal is signal, not data leakage.

Level-Up Roadmap

| Level | Must-have | Bonus signal |

|---|---|---|

| Analyst | Flawless models, tight diligence modules, crisp exhibits | Own a mini-workstream; automate a recurring analysis |

| Associate | End-to-end workstream ownership; advisor orchestration | Source a live deal or prove an operating lever with measured ROI |

| Senior Associate | Lead modules; mentor juniors; draft the IC narrative | Credible origination pipeline; KPI cadence you installed at a portco |

| Vice President | Run full processes; pattern recognition in diligence; CEO trust | Repeatable sourcing engine; board-quality materials that de-risk IC |

Backgrounds That Convert

- IB / Consulting: classic feeders—prove you owned more than tabs and slides by showing workstream leadership and decisions.

- Operators (finance, revenue, product): bring KPI wins and change management; translate operating proof into underwriting logic.

- Big 4 TAS / QoE: advantage on quality of earnings and downside scenarios; add independent modeling reps to round it out.

- Data / Analytics: cohorting, pricing experiments, GTM instrumentation—connect the dots to $ outcomes and cash flow.

School names help. Measurable impact helps more. Bring artifacts.

Common Pitfalls to Avoid

- Vague attribution: “supported a deal” ≠ owned a workstream. Be specific about inputs, decisions, and results.

- Model-only profile: great tabs, no process or operating evidence. Add diligence logs and KPI work to balance the story.

- Confidentiality misses: sharing sensitive details kills trust. Redact and summarize instead.

- Spray-and-pray networking: volume without value. Build targeted banker/founder loops and track hit rate.

30-Day Prep Sprints (if you’re breaking in)

- Week 1: rebuild an LBO from scratch; write a 1-page IC “so what” for a recent buyout.

- Week 2: draft a redacted diligence memo and a downside case; practice a 10-minute IC pitch.

- Week 3: assemble a mini KPI dashboard from a public comp; propose three value-creation levers.

- Week 4: build a banker/founder outreach list; secure five warm intros and track hit rate.

Convert these outputs into your Proof Pack and bring them to interviews.

Private Equity vs. Investment Banking Compensation (2026)

For junior finance pros, moving from investment banking (IB) to private equity (PE) is a classic pivot. Here’s the head-to-head so you can decide with eyes open.

The Head-to-Head Comparison

- Compensation: PE associates typically earn ~20–40% more total cash than IB associates at similar seniority. The gap widens at VP/Principal when carry enters the picture.

- Lifestyle & workflow: IB = high, steady grind tied to clients and deadlines. PE = spike-y peaks around live deals and portco fire drills; calmer between cycles.

- The work itself: IB builds market breadth and process muscle. PE pushes ownership thinking—underwriting judgment, operating levers, and long-term value creation.

- Career progression: IB has a structured ladder, but MD slots are scarce. PE often reaches meaningful equity participation sooner, with real performance gates.

- Risk & reward: IB pay is predictable (salary + bonus). PE cash is higher on average but more variable; long-tail wealth depends on realized carry.

Juniors vs. Seniors: Two Timelines

Juniors (illustrative): A 3rd-year IB associate might earn ~$275k with ~80+ hour weeks. A comparable PE associate could clear $350k+ with more variance tied to fund/deal outcomes.

Seniors: At Principal/MD, cash matters less than realized carry. Bank MDs can earn very high cash in peak years, but they rarely share a profits pool. In PE, a few clean exits across vintages can dwarf a decade of salary + bonus.

How to Choose: Quick Checklist

- Your goal: Market/client breadth → IB. Ownership & ops depth → PE.

- Risk appetite: Prefer certainty → IB. Comfortable with long-term upside → PE.

- Timeline: Value a structured path → IB. Want earlier equity participation → PE.

- Fit: Consider local ecosystems (deal flow, portcos, clients) and lifestyle realities—not just year-one cash.

Numbers are directional bands; outcomes vary by firm, city, sector, and timing.

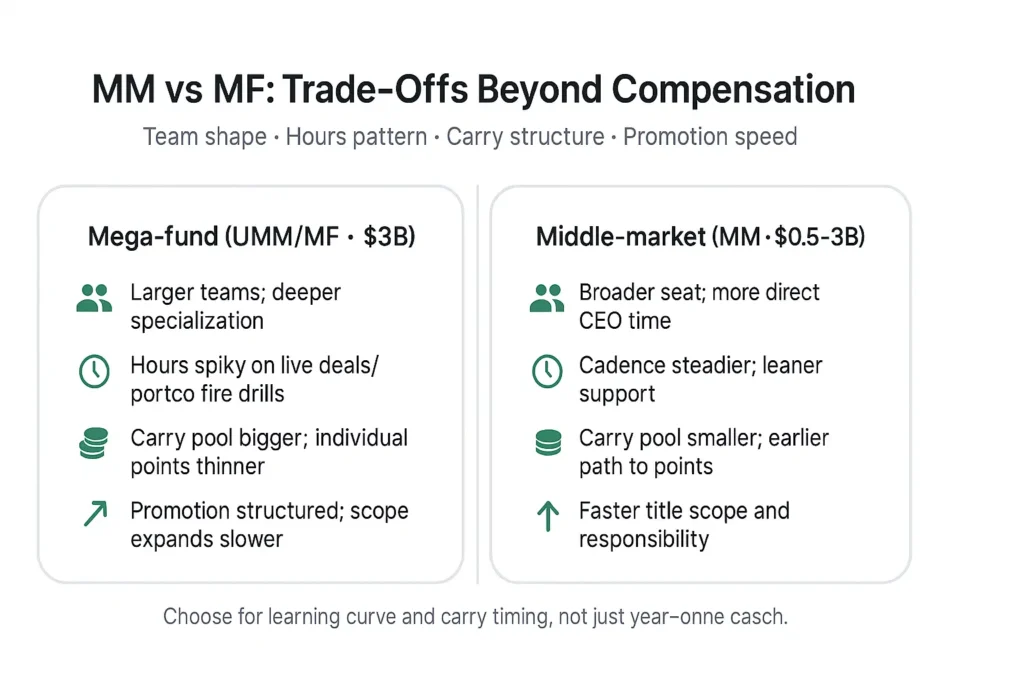

MM vs. MF: The Trade-Offs Beyond Compensation

- Team & role: Mega-fund teams are larger and more specialized, so you’ll go deep in a specific area. Middle-market roles are broader, with more direct CEO interaction and earlier ownership of full workstreams.

- Lifestyle: MF hours are spiky, clustering around live deals and portco “fire drills.” MM can be more predictable, but teams are leaner so there’s less support.

- Career & equity: Promotion and responsibility often come faster in the middle market. Mega-funds offer bigger carry pools, but your individual slice (carry points) is typically thinner.

- Bottom line: Choose based on the learning curve you want and when you hope to see carry—not just year-one cash compensation.

Exit Opportunities & Career Paths After Private Equity

PE skills translate across finance. Here’s where professionals typically land:

| Path | Why PE Skills Fit | Comp Shape |

|---|---|---|

| Hedge Fund | Underwriting rigor, catalyst mapping | Cash-heavy, performance bonus |

| Growth/VC | Pattern spotting, founder empathy | Lower cash, longer carry |

| Portfolio Exec | KPI cadence, value playbooks | Cash + meaningful equity |

| Corp Dev | Deal process, integration | Corporate comp + RSUs |

| Entrepreneurship | Sourcing engine, equity story | High variance, equity-driven |

How to Maximize Private Equity Compensation

Your Compensation Playbook

- Develop a specialized edge: be the go-to on operating levers (pricing, GTM, margin), digital/analytics, or a sector where your fund hunts. Specialists get paid.

- Translate work into dollars: tie projects to KPI lift (ARR growth, cash conversion, churn, gross margin). Log wins for review and IC.

- Build a sourcing machine: banker/founder loops, CRM hygiene, and a monthly hit-rate to qualified leads.

- Own the process: clean IC materials, on-time closes, and a crisp 100-day plan with measurable owners and dates.

- Board-ready communication: summarize risk, alternatives, and “so what” in one slide; this moves bonuses up the band.

Sourcing Math (what good looks like)

| Funnel stage | Target cadence | Quality bar |

|---|---|---|

| Top-of-funnel intros | 40–60/mo | Warm intros & repeatable lists, not spray-and-pray |

| Qualified screens | 8–12/mo | Clear “why us / why now,” quick disqualify discipline |

| LOIs | 1–2/quarter | Underwriting edge identified; CEO trust established |

| Closes | 2–4/year (team-dependent) | Clean processes; integration plan ready at sign |

Numbers are directional. Quality beats quantity, and your fund’s strike zone narrows or widens the funnel.

Timing Your Career Moves

- Time the calendar: move after bonus and realized carry distributions to avoid forfeits.

- Time the fundraise: negotiate points when a new fund is forming and the pie is being sliced.

- Time your story: go to market right after exits or measurable portco wins; that’s when your narrative is hottest.

Negotiation Levers (total package)

- Title & scope: written remit (sourcing %, IC role) with a date-certain first review.

- Bonus mechanics: target + floor + discretionary upside language.

- Carry: points of the pool, vesting schedule (cliff + straight-line), vesting credit for prior service, and acceleration on termination without cause.

- Distribution terms: waterfall (European vs. deal-by-deal), escrows/reserves, and clawback obligations.

- Co-invest: access, caps, and whether employee allocations are fee/carry-free.

- Bridging economics: sign-on/relocation to offset forfeits; garden-leave clarity; start date relative to payouts.

Before signing, run the math in Carry 101 and confirm definitions in the LPA/agreements. The fine print is the comp.

Offer Deconstruction (worksheet)

| Term | Why it matters | What “good” looks like |

|---|---|---|

| Base / Bonus target | Cash today | Target + floor; clear drivers and timing |

| Carry points | Wealth engine | Documented points; path to step-ups at milestones |

| Vesting | When you earn it | 1-yr cliff + straight-line; credit for prior service |

| Acceleration | Downside protection | Without-cause = partial/full vesting acceleration |

| Distribution method | Timing of payouts | European vs. deal-by-deal; escrow/reserve clarity |

| Clawback | Payback risk | Cap, duration, and net-of-tax treatment spelled out |

| Co-invest | Additive upside | No fee/carry; clear caps; financing option if offered |

| Non-compete / Garden leave | Mobility & timing | Scope, geography, duration proportionate |

| Start date vs. payouts | Don’t forfeit | After bonus/distribution or bridged with sign-on |

| Review cycle | Raises & title | Date-certain review; criteria tied to outcomes |

Conclusion

Private equity in 2026 is dynamic and brutally competitive. Cash (base + bonus) pays the bills; carry builds the balance sheet—especially at senior levels. The real edge comes from picking the right seat for your learning curve, executing cleanly, and lining up your story with the fund’s realization cycle.

Private equity in 2026 is dynamic and brutally competitive. Cash (base + bonus) pays the bills (and yes, the overpriced lattes); carry builds the balance sheet—especially at senior levels. The real edge comes from picking the right seat for your learning curve, executing cleanly, and lining up your story with the fund’s realization cycle.

Navigating PE takes more than technical skill. You need resilience, adaptability, and the ability to build relationships without torching bridges when you’re sleep-deprived. If you can handle the grind, the upside and career optionality are second to none.

Whether you’re an analyst getting started or a seasoned pro mapping a partner track, use this guide to make sharper decisions, negotiate like an adult, and build a durable career in a field where the money is very real—and so is the stress.

Timing Your Move (final recap)

- Move post-bonus: let the cash land before you walk. Avoid preventable forfeits.

- Negotiate pre-fundraise: push for points when a new fund is forming and the pie is being sliced.

- Don’t leave before a distribution: know the payout calendar. Confirm vesting credit and distribution timing so you’re not stepping over dollars to pick up dimes.

More detail in How to Maximize Compensation. Ranges are directional; your outcome swings with strategy, city, and timing.

📋 The Pre-Signature Checklist

Your total comp is a bundle of levers. Optimize the package—not just the base:

- Title & scope: SA vs. VP (or higher) with remit in writing (sourcing %, IC role) and a date-certain first review.

- Bonus mechanics: target + floor + discretionary upside language and payment timing.

- Carried interest: points in the carry pool, vesting schedule (cliff + straight-line), vesting credit for prior service, and acceleration if terminated without cause.

- Distribution terms: waterfall method (European vs. deal-by-deal), escrows/reserves, and clawback treatment.

- Co-invest: access, caps, and whether employee allocations are fee/carry-free (and any leverage facility).

- Bridging economics: sign-on/relocation to offset forfeits; start date set relative to payouts.

- Restrictions: non-compete / garden leave—scope, geography, and duration proportionate to the seat.

- First review cycle: date-certain performance/title review tied to measurable outcomes.

Before you sign, run the math in Carry 101 and sanity-check terms against the LPA/agreements. The fine print is the comp.

Frequently Asked Questions (FAQs)

Quick Answers

Let’s be clear: there’s no single “average” salary in private equity. Compensation varies dramatically by your level, fund size, city, and performance. As a quick guide, all-in cash compensation for Associates typically lands around $275k–$350k at middle-market firms and $325k–$450k at mega-funds. VPs often clear $450k–$700k in cash. Senior partners can earn $900k–$2M+ in cash, with realized carry lifting their total earnings far higher.

At the junior levels, PE associates typically out-earn their investment banking peers by 20–40% in cash. At the VP level and above, private equity’s carried interest becomes the main driver of its massive long-term pay advantage. In short, IB offers more predictable annual pay, while PE offers higher upside with more variance.

Carry is typically introduced at the Vice President (VP) level. While some firms are experimenting with granting small amounts to Senior Associates after 2-3 years, this is a firm-specific perk, not the industry standard. Remember, carry usually vests over 4–6 years and only pays out on realized exits, not on-paper gains.

The core skills are the price of admission: financial modeling, deal diligence, process management, and clear communication. The skills that truly set you apart are understanding operational levers (like pricing, GTM strategy, and margins), driving a performance-focused KPI cadence with portfolio companies, and building a genuine sourcing engine. At the end of the day, relationship judgment beats raw hours.

Deliver tangible results by tying your work to KPI improvements, build a network that generates proprietary deal flow, and develop a true operational edge. Most importantly, negotiate the entire package: carry points, vesting schedule, acceleration clauses, distribution terms, and co-investment rights.

Carry Mechanics in 60 Seconds

The back-of-the-envelope formula is:

Payout ≈ (Fund Size × (MoIC − 1)) × GP Carry % × Your Points

(MoIC stands for Multiple on Invested Capital). This simple formula ignores fees, hurdles, and other complexities, which are covered in our full Carry 101 guide.

A European waterfall (fund-as-a-whole) pays out later, but the calculation is cleaner. A deal-by-deal waterfall can pay out earlier but is often subject to a clawback, meaning if later deals lose money, you may have to give back some of your earlier distributions.

The short answer? Almost never. Consider it a rare bonus if you’re a Senior Associate who gets a few points, not a baseline expectation. However, they may receive the opportunity to co-invest in the company’s equity.

Sources & Notes

Ranges reflect aggregated recruiter conversations, public survey snapshots, and anonymized datapoints across 2024–2025. Cash comp = base + annual bonus. Carry shown separately due to vesting/realization timing. Geography, strategy, vintage, and performance create wide dispersion—treat ranges as directional bands.

Last updated: February 2026