77% of U.S. buyouts in Q1 2025, or nearly 8 out of 10 deals, happened in the middle market, and ~70% were below $500M in enterprise value per PitchBook’s latest data. This stat blows up the “mega-fund or bust” myth that resonates through the deep, dark Wall Street Oasis forums, and points to middle-market private equity careers as a potential game-changer for anyone trying to break in.

Therefore, ambitious candidates (especially those of us not on the Wharton-to-KKR train) should see this market shift as a transformative opportunity and an asymmetric bet on their own career.

I’d still be sweating away (and probably twice divorced) in banking if I didn’t consider the MM. While headlines chase billion-dollar closings, the real volume, and the most tangible opportunity, is in the trenches of middle-market private equity. It’s here, where juniors are often handed the model vs. the coffee, and can be put on a fast track to carry.

Most importantly, whether you’re a scrappy first-gen financier fighting to break in or a Goldman analyst who just missed on-cycle, your highest-probability, highest-growth entry point into private equity today isn’t at Blackstone or KKR, but in the middle market (at a firm you might not have even heard of… yet).

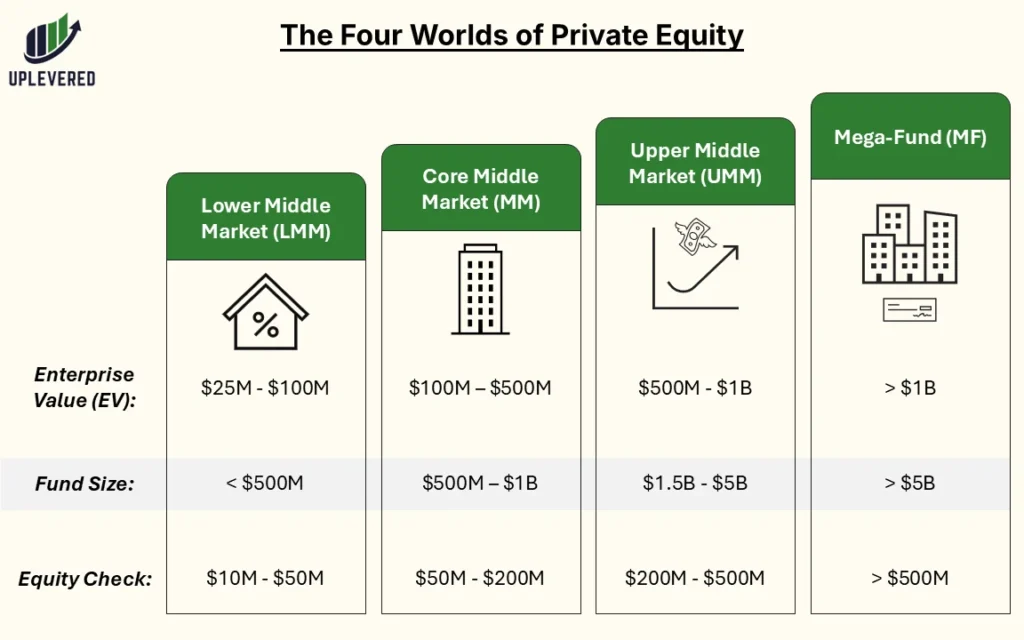

The Four Worlds of Private Equity: A Career Guide

Let’s be real: not all private equity firms are creating equal. It’s made up of four very different worlds, each with its own rules, resources, culture, and resume weight.

While the boundaries are hazy and often brutally contested by VPs at overpriced cocktail bars, understanding these segments is crucial. Read on below to see what you’re really signing up for:

The Lay of the Land

The chart outlines the generally accepted PE universe. The core metric to focus on is Enterprise Value (EV), as it pretty much dictates everything else.

| Tier | Enterprise Value (EV) | Typical Fund Size | Typical Equity Check |

| Lower Middle Market (LMM) | $25M – $100M | < $500M | $10M – $50M |

| Core Middle Market (MM) | $100M – $500M | $500B – $1.5B | $50M – $200M |

| Upper Middle Market (UMM) | $500M – $1B | $1.5B – $5B | $200M – $500M |

| Mega-Fund | > $1B | > $5B | > $500M |

(Source: Pitchbook Report Definitions & UpLevered Estimates)

Real Talk: Don’t Stress the Size Band

Make sure not to get so carried away with the perfect fund / firm size that you miss your chance to get in the door. Breaking into private equity is half the battle.

Once you have “Private Equity Associate” on your résumé, you have the leverage and credibility to lateral to your dream fund down the road.

As Sun Tzu probably said, “First, win the battle. Then, you can win the war.” (and don’t worry, even if you’re LMM, you can still put “Private Equity Associate” on your Hinge profile 😉)

Why This Chart Defines Your Career

Forget the deep, dark Wall Street Oasis talk about prestige for a minute. These numbers directly translate into the experience you’ll get, the skills you’ll build, and how fast you’ll advance. For many, middle-market private equity careers can provide benefits vs. mega-funds.

Deal Size → Seat at the Table

Generally, smaller deals mean greater responsibility, faster. The math is simple: on a $75M LMM buyout, the firm genuinely can’t afford to have you just run analyses. You’re more likely to be in the room, sit on boards, and work directly with management on operational changes. This can be a blessing or a curse, depending on your personality / interests.

Fund Size → Surface Area of Learning:

Beyond the deal itself, sub-$1B funds can’t afford siloed specialists like MFs. You will often be a generalist in the truest sense of the word (especially towards the LMM end of the spectrum) and be thrown into the fire to learn the entire deal lifecycle. On any given day, you will:

- Build the model from scratch (once you’ve shown you’re no longer a #REF! risk)

- Help draft entire sections of the investment committee memo

- Manage the diligence vendors (who will hopefully buy you drinks)

- Spend your evenings and occasional weekends tracking portfolio company KPIs

- Potentially be asked to help with sourcing (shop dependent on wether this is just industry research vs. telemarketing like expectations)

But hey, don’t worry! It’s like an MBA (without the vacations) 🙂

Team Structure → Visibility = Velocity

Ultimately, on a lean middle-market team, your work is pretty much impossible to ignore. Every diligence request, model, and memo has your blood, sweat, and tears on it. Partners notice, LPs notice, and, if you do your job right, the people that promote you notice. That’s a much harder feat to pull off on a 40-associate mega-fund floor, which tend to be structurally more top-heavy as well.

UpLevered Takeaway: Tilt the Odds

If you have a shot at a mega-fund, 100% take it. These firms top all tier lists you may see for a reason. You’ll likely know (and hopefully still have your hair) if you fall in this elite group.

For everyone else, clinging to the “mega-fund or bust” myth is a lottery ticket that can crush you mentally. The winning strategy is to stack the odds in your favor. This makes MM the ideal platform to develop those skills (and even potentially earn carry before you’re 30) and /or the option to lateral to your dream fund.

Choose the path that maximizes your reps and forges you into a genuine investor. Once you’re in the door, it’s time to run up the score – Dr. Seuss would love me for that.

Where the Action Is: Following the Deals & The Dollars

Let’s dive into the numbers.

In Q1’25, nearly 80% of all U.S. buyouts took place below the $1B Enterprise Value mark, accounting for 43% of total capital invested. Note that historically, the middle market’s share of total value has generally been even stronger, representing nearly 60% of all capital deployed through 2023 and 2024.

To put that in perspective, volume is critical for getting reps / deals on your resume, and the majority of capital being deployed to that sector means there are a lot of meaningful / bigger deals to learn from.

So MM, may not just be the a side show – it kind of is the show.

Follow the Deals → Why Volume Beats Value

As the data states, most transactions, and by extension, deal teams, associate roles, and learning opportunities, are concentrated in the middle and lower-middle markets.

Additionally, these aren’t just simple buyouts of the local HVAC guy sponsoring your little league team… The volume includes complex deals like corporate carve-outs, which made up nearly 10% of all middle-market activity in Q1 2025.

For your investing experience, the math is simple: More deals = more time to shine.

Follow the Money → Fundraising & Dry Powder

Deal activity is a snapshot of today (like what you learned about the BS!). However, fundraising points to the future, like an over-priced crystal ball.

And the future is flowing directly into the middle market. Even in the “tough” 2024 fundraising environment, middle-market funds successfully drew the majority (55%) of all buyout fundraising capital.

This success has led to a massive capital overhang. As of late 2024, middle-market PE managers were sitting on a record stockpile:

- $546B in “dry powder” (unused equity to be deployed)

- This represents over 53% of every U.S. PE dollar available

For you, that immense pressure to deploy capital translates into one thing: outsized demand for bright-eyed, hungry associates who can source, model, and close.

(Note: All statistics in this section are sourced from the PitchBook Q1 2025 US PE Middle Market Report.)

The UpLevered Thesis: Why Middle-Market Private Equity Careers Can Be the Smartest Play

The data shows the middle market is where the deals are. But more importantly, it can be the higher-probability path that allows you to shine bright like a diamond while building a better, faster, and more durable career. Here’s why:

1. More Reps, Faster Growth

The single most important factor in your early career development is 1). the number of “reps” you get and 2). the type of reps you get. At a mega-fund, you might spend two years on a single, massive take-private of Japan’s largest tofu manufacturer. While, if you were working in the MM during that time, you would have rolled up a 3 – 5 of the Midwest’s porta-potty dealers. Thus, often making the faster deal cadence outweigh the more specialized experience gained from MFs.

2. Real Responsibility, Not Just “Reviewing”

Beyond just deal quantity, middle-market firms often run lean (while you’re working on a Friday at 9pm, you may argue too lean in fact). A MM associate isn’t just a small cog in a giant machine; you are the machine. You own the model (#REF!-depending). You coordinate with the lawyers and accountants. You draft entire sections of the investment committee memo. You do a lot.

3. A Better Path to Partner

The career path at mega-funds is notoriously narrow at the top. Middle-market firms, on the other hand, are often in growth mode and more likely to promote from within without having to rely too much on your LP family member pushing you to VP. The fact that the pyramid isn’t as steep makes your contributions far more visible.

4. Hustle Beats Pedigree

Finally, a crucial point for those who missed the [insert big city wealthy suburb] high school investment club to Goldman pipeline: mega-funds have an extremely rigid and finely vetted recruiting pipeline. The middle market is different. They hire off-cycle and tend to be less selective, often valuing hustle and a proprietary angle.

The Money: A Look at Comp & Career Trajectory

Let’s be honest: we all want to get paid. And yes, on a headline basis and with respect to total career earnings potential, mega-funds win. But the story is more nuanced.

Based on the latest 2024-2025 compensation surveys, here’s a realistic look at all-in cash for a PE Associate in North America:

| Firm AUM | Role | All-in Cash (Mean) |

| Lower Middle Market (<$1B) | Associate | ~$260k |

| Middle Market (<$2B) | Associate | ~$300k |

| Upper Middle Market ($2B – $5B) | Associate | ~$340k |

| Mega-Fund (>$10B) | Associate | ~$400k |

(Sources: Heidrick & Struggles 2024 Private Equity Compensation Survey, Odyssey Search Partners 2024 Private Equity Compensation Study)

While the mega-fund premium is real, don’t worry – I’m pretty sure you’ll be outperforming 99.9% of the global population at any firm size.

Additionally, focusing only on starting salary is a rookie move. Your early-career compensation is pennies in comparison to two far more powerful outcomes: 1). the enormous wealth from (what Kamala would call undertaxed) long-term carry or. 2). the lifelong access that comes from a prestigious brand on your resume.

The ~$100k difference, therefore, shouldn’t be the deciding factor. The real question is: which path are you optimizing for?

For those playing the long game for prestige, seeking a golden ticket to business school, or the credibility to raise your own fund / start your own venture, the mega-fund allure is powerful and logical. Let’s break down why.

The Devil’s Advocate: Why the Mega-Fund Allure is Real

Let’s be realistic. The path to a mega-fund is paved with gold and heartache for a reason. Ignoring the powerful advantages of playing in that arena would be doing my industry an injustice. While I argue the MM is the smarter play for most to break into PE and build a durable career, here’s why someone would intelligently choose the opposite:

Unmatched Prestige & The “Golden Handcuffs” of Exit Ops.

Having Blackstone or KKR bolded on your resume is a lifelong asset. The top-50 or so PE firms give a signal that opens doors vs. MM firms.

If your goal is to waltz into Harvard Business School, get people to give you their money (i.e. search fund, your own fund), or move into a cushy corporate strategy role, the mega-fund brand provides the most direct (brutally competitive) path.

Exposure to Unparalleled Complexity

A $15B take-private of a multinational corporation is a different animal than a $150M HVAC roll-up. At a mega-fund, you’re exposed to the absolute cutting edge of financial engineering, cross-border M&A, and complex capital structures.

The learning is less about the whole deal and more about mastering a highly specialized, incredibly valuable sliver of high finance.

A World-Class Network

Additionally, the contacts you may butt dial after two years at a mega-fund include future titans of the industry, hedge fund legends, and top-tier bankers and lawyers.

The sheer institutional power of that network provides an undeniable career boost (and possibly invites to yacht parties in Southern France), which is something a regional middle-market firm simply cannot replicate at the same scale.

So, the choice isn’t just about money. It’s a strategic bet on where your background can take you and what you value more early in your career: the tangible reps of the middle market vs. the brand equity of the mega-fund.

Real-World Middle-Market Private Equity Careers Snapshot: Anatomy of a $150mm HVAC Roll-Up

To see how this all comes together, let’s walk through a good ‘ol deal at a core middle-market fund. You’re a second-year associate, still not burnt out, and with a surprisingly stable relationship.

Sourcing & Initial Screen: A regional business broker, cultivated by you or your firm’s lean business development team, sends over a teaser: a family-owned HVAC services company with $15M in EBITDA. You spend the afternoon building a quick financial spread or LBO model to see if the numbers work. As I have many times witnessed, this may involve you transcribing a scribbly scanned pdf into excel :).

Diligence & Modeling: Working with your VP, you take the lead on building a more detailed operating model. You’re buried in the data, trying to answer all of your MD’s / Directors many requests about customer concentration, how they actually make money, and why anyone would buy them. You’re also looped into key calls, listening as the accounting firm presents its findings from the Quality of Earnings (QoE). *Staying awake during these is key

Investment Committee You own entire sections of the investment memo, like the “Base Case Analysis” and “Company Overview”. When the deal goes to committee, you’re in the room or have been ready to assist in defending your model’s key assumptions and speak to the underlying data that supports your team’s thesis, or you were an instrumental part of preparing the case.

Portfolio Monitoring Post-close, the work continues. You’re a key contact for the portfolio company’s new CFO, responsible for helping them:

- Model the financial impact of acquiring bolt-on targets you identified

- Track and assess synergy realization

- Monitor performance against your underwriting model’s targets

- Hopefully not be asked why we are losing money

Frequently Asked Questions – Middle-Market Private Equity Careers

While there’s no single definition, it generally refers to firms investing in companies with enterprise values between $25 miillion and $1 billion. This is often broken down into the Lower Middle Market ($25M – $100M), Core Middle Market ($100M – $500M), and Upper Middle Market ($500M – $1B).

Yes, it’s highly competitive. However, the path is often more accessible than mega-funds, especially for candidates with non-traditional backgrounds. Middle-market firms value relevant operational or transaction experience and are more open to off-cycle hiring.

An associate at a core middle-market fund can expect an all-in cash compensation of around $200k – $300k. However, this is heavily dependent on the firm and location. While this is less than a mega-fund, the hands-on experience and career trajectory can offer greater long-term value.

Conclusion: Your Move

Finally, don’t fall for that “mega-fund or bust” mindset lurking on Wall Street Oasis. The data makes it clear: the middle market is the engine of the private equity industry and is often the more definitive chance at building your investing career.

If you’re ready to send off those Blackstone day-dreams for reps on the MM frontline, download our MM-focused résumé template to see how to best position your experience for breaking in. For a complete A-to-Z plan and overview of the industry / recruitment processes, check out our definitive break into private equity guide.